NPS (National Pension System) – Tax Benefits

Tax and death are inevitable. Section 80C comes to the rescue of the majority. Section 80D provides further reprieve. Like the frog in the well, we are generally not aware of sections 80CCD(1B), 80CCD2. To know these sections, we don’t need to read the fine prints of NPS (National Pension System). They are readily available. Let us dive deep into the tax benefit of NPS investment.

Retirement is the least focussed financial goal for us. Even though products like NPS nudge us to initiate our journey towards relaxed retirement, we have not made the effort to understand its impact on our pockets in the present as well as in the future.

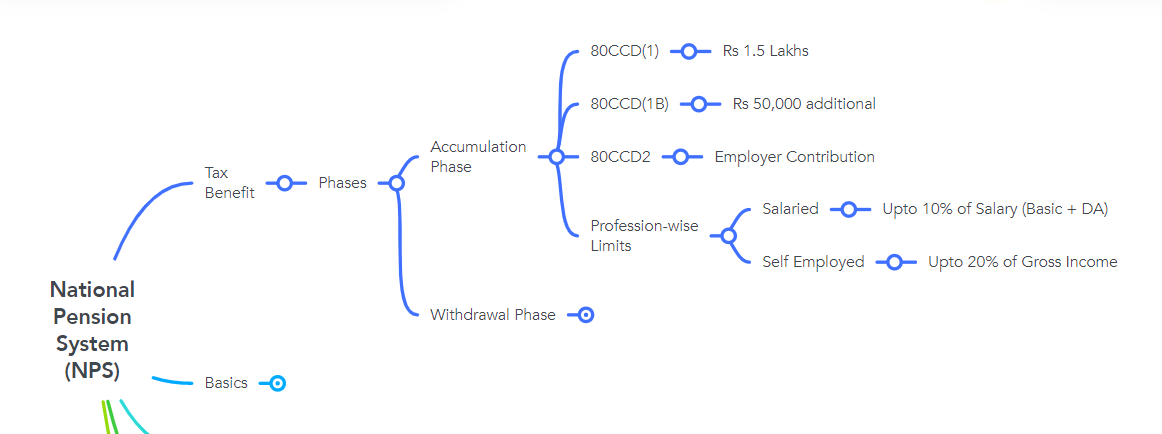

Tax Benefit of NPS investment in Accumulation Phase

NPS Tax Benefit – Accumulation Phase

Section 80CCD(1) allows us to invest Rs 1.5 lakhs in NPS to get the deductions under section 80C. Yes, this is the very section that made us invest in ELSS mutual fund, life insurance, provident fund, 5 years fixed deposit, etc. Till here it is just a very normal investment.

The magic happens when we come to know that we can further invest Rs 50,000 in NPS (over and above Rs 1.5 lakhs under section 80C) to increase our tax saving under section 80CCD(1B). For someone in the 30% tax bracket, it saves him Rs 16,666 every year.

If you are a salaried employee, you can get your salary restructured in a manner that your employer invests 10% of your salary (Basic + DA) in NPS under section 80CCD2. This amount can further be claimed as a deduction from taxable income. The upper cap is a whopping Rs 7.5 lakhs per annum.

A self-employed individual can claim tax deduction up to a maximum of 20% of gross annual income for the amount invested in NPS under section 80CCD(1) and 80CCD(1B).

This brings us to the close of tax benefits in NPS during the accumulation period. Let us now understand how is it useful during the withdrawal phase.

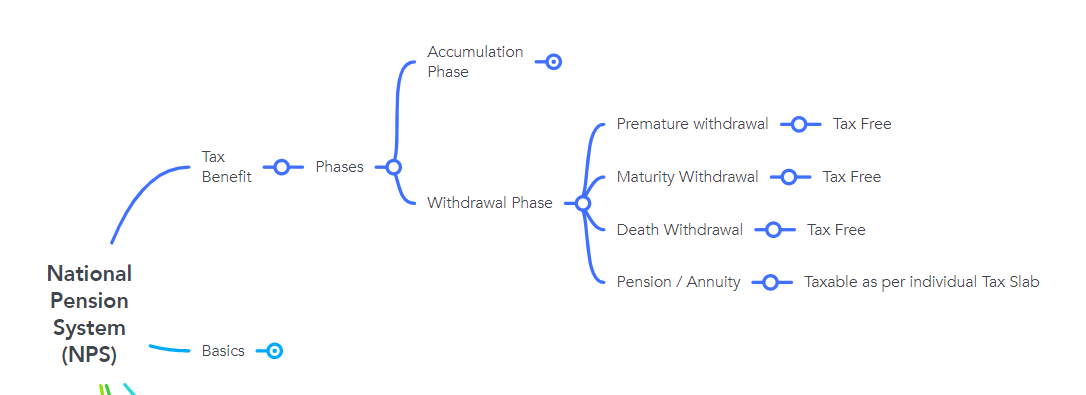

Tax Benefit of NPS investment in Withdrawal Phase

NPS Tax Benefit – Withdrawal Phase

The following withdrawals are tax-free:

- If you are doing a premature withdrawal from the NPS corpus (up to the specified limit as prescribed under NPS, which we will discuss in another article/section) before the maturity age of 60 years is reached.

- The withdrawal of up to 60% of the corpus on maturity after the age of 60 years.

- On the death of the investor, the full amount that is paid to the nominee.

The pension that you get on a regular basis from the annuity amount is added to your annual income and taxable as per your applicable tax slab. If the above-mentioned pension is your only income, the initial Rs 2.5 lakhs is not taxable as per the tax rules. Further, a standard deduction of Rs 50,000 is applicable.

Exempt Exempt Exempt

To sum it up, NPS is a magnificent tool to prepare for retirement as well as save tax outgo. The tax benefit is threefold:

- Investing phase – TAX-FREE.

- Fund growth phase – TAX-FREE.

- Withdrawal phase – TAX-FREE.

This makes it one of the very few instruments that are under the EEE category – Exempt Exempt Exempt category. The tax benefit of NPS investment is huge

Do not let go of this opportunity to rationalise your tax component. You have worked hard for every penny. When legal methods are provided for us, not utilising them is like burning our money ourselves. Write your questions below and share this with your friend. If he benefits, he may treat you soon as a reward for the help.

Recent Comments